Financial Freedom Tips are becoming more important than ever as millions of Americans look for smarter ways to manage money, reduce debt, and build long-term wealth. Rising living costs, inflation, and financial uncertainty continue to pressure households across the United States. As a result, more people now want practical strategies that can improve financial security and reduce money-related stress.

Moreover, financial freedom does not simply mean becoming extremely wealthy. Instead, it means having enough savings, investments, and income to support your lifestyle without constantly worrying about bills or debt. Some people achieve financial freedom through investing, while others focus on budgeting, passive income, or debt reduction. Consequently, every financial journey looks slightly different.

What Is Financial Freedom?

Financial freedom means having enough financial stability to make life decisions with greater flexibility and confidence. Instead of depending completely on paycheck-to-paycheck income, financially secure individuals build systems that support long-term stability.

Financial freedom often includes:

- Emergency savings

- Low or no debt

- Long-term investments

- Passive income streams

- Retirement planning

Although financial goals differ for every household, most people want greater control over their money and future.

Why Financial Freedom Tips

Money problems can create stress, anxiety, and uncertainty. However, better financial habits often improve both financial stability and peace of mind.

Financial freedom may help you:

- Handle emergencies confidently

- Reduce financial stress

- Avoid high-interest debt

- Retire more comfortably

- Create career flexibility

Therefore, financial planning affects much more than bank account balances alone.

Tip 1: Create a Realistic Budget

Budgeting forms the foundation of strong money management. Without understanding spending habits, long-term financial planning becomes far more difficult.

A practical budget should include:

- Housing expenses

- Transportation costs

- Food spending

- Debt payments

- Savings goals

- Entertainment expenses

Budgeting tools such as:

can simplify expense tracking and financial organization.

Tip 2: Build an Emergency Fund

Unexpected expenses can disrupt financial progress quickly. Consequently, emergency savings remain one of the most important personal finance priorities.

Emergency funds often help cover:

- Medical expenses

- Job loss

- Car repairs

- Home maintenance

Many experts recommend saving:

- Three to six months of living expenses

High-yield savings accounts from providers such as:

may help savings grow faster over time.

Tip 3: Eliminate High-Interest Debt

Debt reduction remains one of the fastest ways to improve financial stability. Credit card interest, personal loans, and payday loans can significantly slow wealth building.

Popular debt payoff strategies include:

- Debt snowball method

- Debt avalanche method

- Debt consolidation loans

Consequently, reducing high-interest debt often improves cash flow and lowers financial stress.

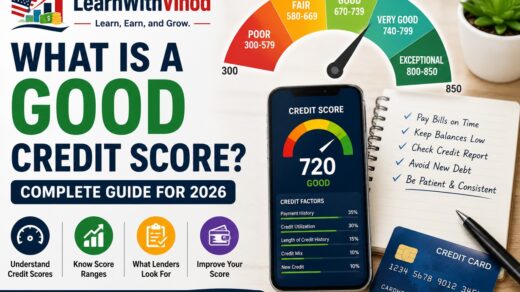

Tip 4: Improve Your Credit Score

A strong credit score can save thousands of dollars over time by reducing borrowing costs.

Higher credit scores may help you:

- Qualify for lower mortgage rates

- Access better credit cards

- Reduce insurance costs

- Improve loan approvals

You can monitor your reports through:

Additionally, paying bills on time remains one of the most effective ways to improve credit health.

Tip 5: Start Investing Early

Long-term investing helps money grow through compound returns.

A=P(1+nr)nt

Over time, investment earnings generate additional returns. Therefore, starting early often creates stronger long-term growth.

Popular investment options include:

- Index funds

- ETFs

- Roth IRAs

- 401(k) plans

- Dividend stocks

Investment companies such as:

offer retirement planning tools and educational resources.

Tip 6: Increase Your Income

Higher income can accelerate financial freedom significantly.

Popular income growth strategies include:

- Side hustles

- Freelancing

- Online businesses

- Investing

- Remote work

Freelance platforms such as:

allow users to generate additional income online.

Tip 7: Build Passive Income Streams

Passive income can strengthen long-term financial independence because income continues flowing with less daily effort.

Popular passive income ideas include:

- Dividend investing

- Rental properties

- Affiliate marketing

- Blogging

- Selling digital products

Although passive income often requires upfront work, it can eventually support greater financial flexibility.

Tip 8: Plan for Retirement

Retirement planning remains essential regardless of age. Many Americans underestimate how much retirement savings they may eventually need.

Retirement accounts include:

Employer-sponsored retirement matching can also accelerate long-term investment growth.

Common Financial Freedom Mistakes

Overspending: Lifestyle inflation can reduce savings and slow investment growth.

Ignoring Investments: Keeping all money in low-interest savings accounts may limit long-term wealth building.

Relying on One Income Source: Diversified income streams provide stronger financial stability.

Delaying Financial Planning: Starting early gives investments more time to compound.

Financial Freedom and Mental Health

Financial stress affects millions of Americans each year. However, organized money management often improves confidence and peace of mind.

Better financial habits may create:

- Reduced anxiety

- Greater flexibility

- Improved stability

- Stronger future planning

As a result, financial freedom supports both financial health and emotional well-being.

Helpful Financial Resources

Readers who want additional financial education can explore trusted resources such as:

These organizations provide financial planning tools, investing education, and consumer guidance.

Frequently Asked Questions

Financial Freedom Tips are strategies that help improve savings, reduce debt, build investments, and strengthen long-term financial stability.

The timeline depends on income, debt, savings habits, and investing consistency.

Yes. Consistent budgeting, investing, and responsible money management can improve financial stability over time.

Passive income is not required, but it can accelerate financial independence.

Increasing income while controlling spending and investing consistently often produces strong long-term results.