If you plan to apply for a credit card, auto loan, mortgage, or apartment rental in the United States, your credit score matters more than you might think. A higher score can help you qualify for better interest rates, lower deposits, and more financial opportunities. But what exactly is considered a good credit score?

In this guide, you’ll learn how credit scores work, what score ranges mean, and how to improve your score over time.

What Is a Credit Score?

A credit score is a three-digit number that reflects how responsibly you use credit. Lenders use it to estimate how likely you are to repay borrowed money on time.

The most widely used scoring model is developed by FICO, and scores generally range from 300 to 850.

The higher your score, the lower your perceived risk as a borrower.

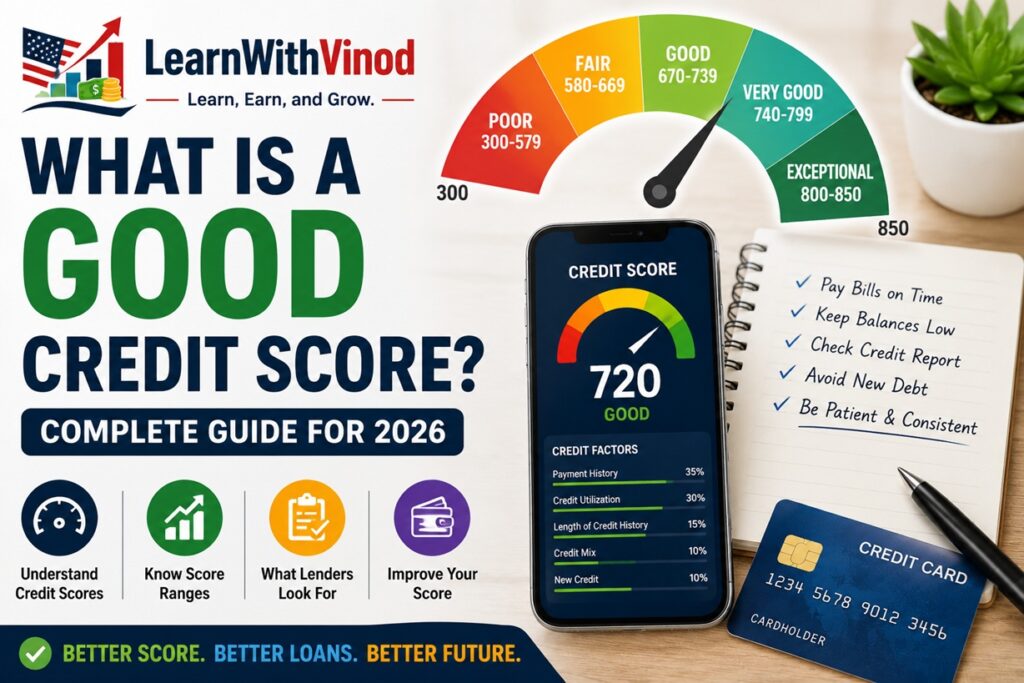

Credit Score Ranges Explained

Here are the standard FICO score ranges used by many lenders:

| Credit Score Range | Rating |

|---|---|

| 300–579 | Poor |

| 580–669 | Fair |

| 670–739 | Good |

| 740–799 | Very Good |

| 800–850 | Exceptional |

A score of 670 or above is generally considered a good credit score.

What Is a Good Credit Score?

A good credit score falls between 670 and 739.

With a score in this range, you may:

- Qualify for many credit cards

- Receive better interest rates

- Obtain higher credit limits

- Improve mortgage and auto loan approval chances

If your score is 740 or higher, you are typically viewed as a lower-risk borrower and may receive even more favorable terms.

Why a Good Credit Score Matters

Your credit score can affect many aspects of your financial life.

Loans and Mortgages

Higher scores usually lead to lower interest rates, which can save thousands of dollars over time.

Credit Cards

A strong score may qualify you for cards with better rewards and lower fees.

Renting an Apartment

Landlords often review credit history before approving applications.

Insurance

In some states, insurers may consider credit-based information when setting premiums.

Utility Deposits

Good credit can reduce or eliminate security deposits.

What Factors Affect Your Credit Score?

FICO scores are based on several key factors:

Payment History (35%)

Paying bills on time is the most important factor.

Credit Utilization (30%)

This measures how much of your available credit you are using. Keeping utilization below 30%, and ideally under 10%, is beneficial.

Length of Credit History (15%)

Older accounts generally strengthen your score.

New Credit (10%)

Applying for several accounts in a short period can temporarily reduce your score.

Credit Mix (10%)

Using different types of credit responsibly may help.

How to Improve Your Score

Improving your credit score takes time, but the process is straightforward.

Pay Every Bill on Time

Set up automatic payments or reminders.

Reduce Credit Card Balances

Pay down cards with high utilization first.

Check Your Credit Reports

Use AnnualCreditReport.com to review your reports.

Dispute Errors

Incorrect late payments or balances can lower your score.

Avoid Too Many Applications

Limit unnecessary hard inquiries.

Keep Old Accounts Open

Long-established accounts support your credit history.

How Long Does It Take to Build Good Credit?

The timeline varies based on your starting point.

- Lowering credit card balances can help within 30–60 days.

- Correcting errors may produce faster results once updated.

- Recovering from missed payments can take several months or longer.

Consistency is the key.

What Is the Average Score in the USA?

The average U.S. score is typically in the good range. However, average figures change over time and vary by source.

The important goal is not to beat the average but to steadily strengthen your own credit profile.

Frequently Asked Questions

Yes. A score of 700 is generally considered good and can qualify you for many financial products.

Yes. A 750 score is considered very good and often results in better interest rates.

Yes, though your options and rates may be less favorable than those available to borrowers with higher scores.

No. Personal credit checks are soft inquiries and do not affect your score.

Pay on time, reduce balances, and correct any errors on your credit reports.

Final Thoughts

A good credit score in the United States generally starts at 670. Reaching and maintaining this range can unlock lower interest rates, better credit card offers, and more financial flexibility.

The best way to build strong credit is to pay on time, keep balances low, and monitor your credit reports regularly.

At LearnWithVinod.com, our mission is simple: