401(k) vs Roth IRA is one of the most important decisions you can make when planning for retirement. Both accounts offer powerful tax advantages, and both can help you build long-term wealth. However, they work in different ways. Therefore, understanding how each account functions can help you choose the strategy that best fits your financial goals.

Moreover, many Americans do not need to choose only one account. In fact, a large number of successful investors use both a 401(k) and a Roth IRA to maximize tax benefits and diversify their retirement savings. Whether you are starting your first job, building your investment portfolio, or catching up on retirement planning, this guide will explain everything you need to know.

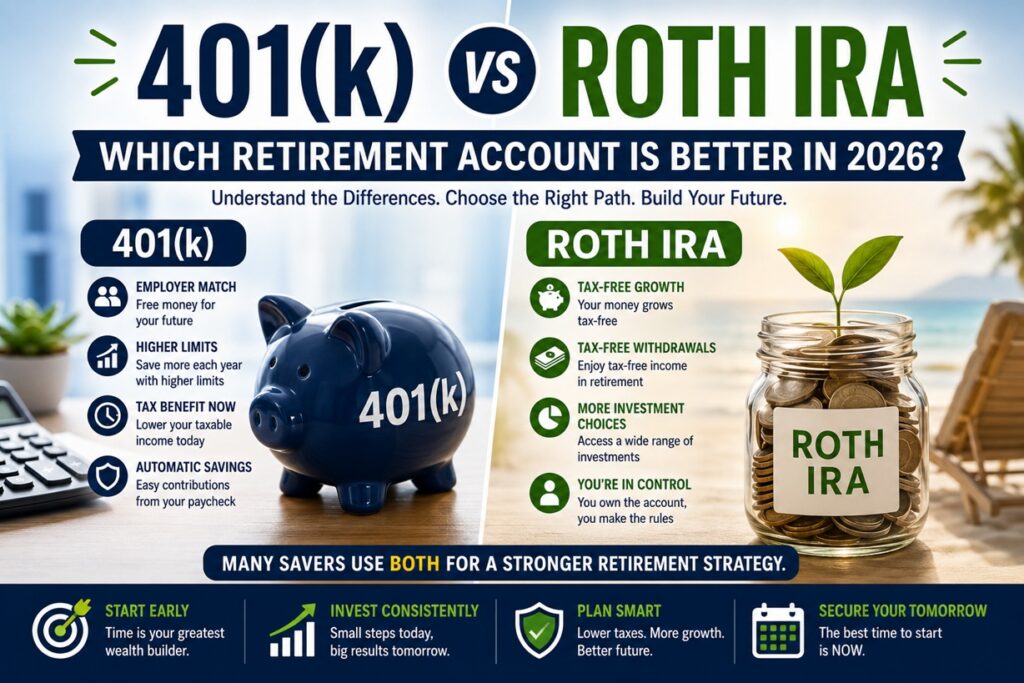

What Is a 401(k)?

A 401(k) plan is a retirement account offered by many employers in the United States. You contribute money directly from your paycheck, and in most cases those contributions reduce your taxable income for the current year.

Even more importantly, many employers match part of your contribution. For example, if your employer matches 50% of the first 6% of your salary, you receive additional retirement savings simply by participating.

Benefits of a 401(k)

- Potential employer matching

- Automatic paycheck contributions

- High annual contribution limits

- Tax-deferred investment growth

Because of the employer match, many financial professionals consider a 401(k) one of the most powerful workplace benefits available.

What Is a Roth IRA?

A Roth Individual Retirement Arrangement (Roth IRA) is a retirement account that you open on your own through a brokerage firm such as Vanguard, Fidelity Investments, or Charles Schwab.

Unlike a traditional 401(k), you contribute money after paying taxes. However, your investments can grow tax-free, and qualified withdrawals in retirement are generally free from federal income tax.

Benefits of a Roth IRA

- Tax-free retirement withdrawals

- Broad investment choices

- Flexible contribution access under IRS rules

- No required minimum distributions during the original owner’s lifetime

As a result, many younger investors and long-term savers prefer the Roth IRA.

401(k) vs Roth IRA: The Key Difference

The main difference between these accounts is the timing of taxes.

401(k)

You often receive a tax break today, but you generally pay taxes when you withdraw money in retirement.

Roth IRA

You pay taxes now, but qualified withdrawals in retirement are typically tax-free.

Therefore, the decision often depends on whether you expect your tax rate to be higher or lower in the future.

401(k) vs Roth IRA Comparison

| Feature | 401(k) | Roth IRA |

|---|---|---|

| Offered By | Employer | You open it yourself |

| Tax Benefit | Tax deduction now | Tax-free withdrawals later |

| Employer Match | Often available | Not available |

| Investment Choices | Limited to plan options | Wide selection |

| Contribution Limits | Higher | Lower |

| Income Restrictions | Usually none to participate | Income limits may apply |

Which Account Should You Choose First?

In many cases, the smartest approach involves using both accounts in a specific order.

Step 1: Get the Full Employer Match

If your employer offers matching contributions, contribute enough to receive the full match. Otherwise, you leave free money behind.

Step 2: Fund a Roth IRA

Next, many investors contribute to a Roth IRA because of its tax-free growth and flexible investment options.

Step 3: Increase 401(k) Contributions

If you can save more, continue contributing to your workplace retirement plan.

Consequently, you can benefit from both immediate and long-term tax advantages.

When a 401(k) Makes More Sense

A 401(k) may be the better starting point if:

- Your employer offers matching contributions

- You want automatic payroll deductions

- You prefer a simple, hands-off process

- You need higher contribution limits

In these situations, the convenience and employer match can make a significant difference.

When a Roth IRA Makes More Sense

A Roth IRA may be a stronger choice if:

- You expect higher tax rates in retirement

- You want tax-free withdrawals later

- You prefer more investment options

- You want greater control over your account

Because of these benefits, many young professionals prioritize a Roth IRA early in their careers.

Can You Have Both a 401(k) and a Roth IRA?

Yes, and many Americans do exactly that.

Using both accounts can provide:

- Greater tax diversification

- More retirement flexibility

- Higher overall savings potential

- Access to a broader range of investments

As a result, combining both accounts often creates a well-balanced retirement plan.

Investment Options Inside Both Accounts

Both a 401(k) and a Roth IRA can hold investments such as:

- Index funds

- ETFs

- Mutual funds

- Bonds

Many beginners choose low-cost index funds that track the S&P 500 because they offer diversification and historically strong long-term growth.

Common Mistakes to Avoid

When comparing 401(k) vs Roth IRA, avoid these common errors:

- Ignoring employer matching

- Waiting too long to start investing

- Leaving money uninvested in cash

- Paying high investment fees

- Contributing inconsistently

Fortunately, a simple and consistent approach can help you avoid these pitfalls.

Frequently Asked Questions

Not necessarily. Each account offers different advantages, and many investors benefit from both.

Yes, if your income and budget allow it.

A Roth IRA can serve as an excellent starting point.

A Roth IRA generally provides greater flexibility.

For many people, the best strategy starts with earning the full employer match and then funding a Roth IRA.

Final Thoughts

When comparing 401(k) vs Roth IRA, there is no single answer that works for everyone. Instead, the best choice depends on your employer benefits, tax situation, and long-term goals.

However, one principle remains universal: starting early matters far more than waiting for the perfect strategy. By contributing consistently, keeping fees low, and allowing your investments to compound over time, you can build substantial wealth and create a more secure retirement.

At LearnWithVinod.com, we simplify personal finance so you can confidently Learn, Earn, and Grow.